If you’re confused about ₹50K rent vs ₹50K EMI in Navi Mumbai, you’re not alone. Thousands of homebuyers in 2026 are asking the same question – should you keep paying rent or start building real wealth through EMI?

₹50K Rent vs ₹50K EMI Navi Mumbai – What’s Happening in 2026?

₹50K Rent vs ₹50K EMI Navi Mumbai – What’s Happening in 2026?

Navi Mumbai is not what it was 5 years ago.

- Infrastructure like Navi Mumbai International Airport is nearing completion

- Metro connectivity is expanding

- Corporate hubs and IT parks are growing

- Demand for housing is rising sharply

This means one thing: Property prices are steadily increasing

Property prices are steadily increasing

At the same time:

- Rents are rising, but not building equity

- Home loan rates have stabilized compared to previous volatility

- Banks are offering competitive deals for buyers

So today, ₹50K is not just a payment —

it’s a financial decision that compounds over time.

₹50K Rent vs ₹50K EMI Navi Mumbai – Simple Comparison Breakdown

₹50K Rent vs ₹50K EMI Navi Mumbai – Simple Comparison Breakdown

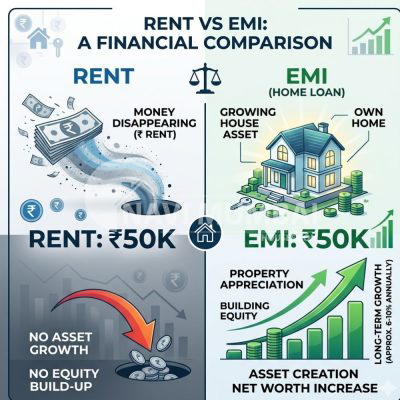

When comparing ₹50K rent vs ₹50K EMI in Navi Mumbai, the difference is not just monthly cost – it’s long-term wealth creation.

Scenario 1: You Pay ₹50K as Rent

Scenario 1: You Pay ₹50K as Rent

- You live comfortably

- No long-term commitment

- Flexibility to move

But…

- Zero ownership

- Zero returns

- 100% expense

After 10 years:

You’ve paid ₹60 lakhs+ And you own nothing

Scenario 2: You Pay ₹50K as EMI

Scenario 2: You Pay ₹50K as EMI

- You own an asset

- Your money builds equity

- Property value appreciates

After 10 years:

You’ve paid roughly the same ₹60 lakhs But you now own a property worth ₹1–1.5 crore (or more)

That’s the difference:

Rent = Expense | EMI = Investment

Rent vs EMI Navi Mumbai – Which Option Builds Real Wealth?

Rent vs EMI Navi Mumbai – Which Option Builds Real Wealth?

Let’s simplify it even more.

Think of Rent Like This:

Think of Rent Like This:

You’re funding your landlord’s wealth.

Think of EMI Like This:

You’re slowly buying your future.

Every EMI you pay:

- Reduces your loan

- Increases your ownership

- Builds long-term security

And in a market like Navi Mumbai, where appreciation is driven by infrastructure, your asset grows even when you sleep.

Real Estate in Navi Mumbai: The Hidden Wealth Engine

Real Estate in Navi Mumbai: The Hidden Wealth Engine

Here’s what most people underestimate:

1. Capital Appreciation

Areas near upcoming infrastructure see 15–40% growth over a few years

2. Rental Income Potential

Even if you move later:

Your property can generate ₹25K–₹50K rent

3. Leverage Advantage

You control a ₹1 crore asset with a fraction of your own money

4. Inflation Protection

Property values rise with inflation — rent just keeps increasing

The Biggest Myth: “EMI Is Too Risky”

The Biggest Myth: “EMI Is Too Risky”

Let’s address the fear directly.

Myth: “EMI is a burden”

Myth: “EMI is a burden”

Reality: Rent is also a fixed monthly burden — but with zero return

Myth: “Property is expensive”

Reality: Prices are rising — waiting makes it worse

Myth: “I’ll buy later”

Reality: Later = higher prices + bigger loan

Real-Life Scenario (You’ll Relate to This)

Real-Life Scenario (You’ll Relate to This)

Imagine two people:

Person A (Renter)

- Pays ₹50K rent for 10 years

- Total spent: ₹60 lakhs

- Net worth from housing: ₹0

Person B (Buyer)

- Pays ₹50K EMI

- Owns a property worth ₹1.2 crore after 10 years

- Loan partially paid off

Same monthly outflow Completely different financial future

This is exactly how wealth gaps are created — silently.

This is where most people stuck in the rent vs EMI Navi Mumbai dilemma make the wrong financial decision.

Rent vs EMI Navi Mumbai – Emotional and Lifestyle Impact

Rent vs EMI Navi Mumbai – Emotional and Lifestyle Impact

Let’s go beyond numbers.

Owning a home gives you:

- Security — no landlord pressure

- Stability — long-term planning

- Pride — it’s YOUR space

- Legacy — something you pass on

Renting gives you comfort.

Ownership gives you control over your future.

According to the Reserve Bank of India, home loan rates directly impact how much EMI you can afford in 2026.

When Renting Still Makes Sense

When Renting Still Makes Sense

To be fair – renting is not “bad.”

It works if:

- You’re unsure about staying long-term

- Your income is unstable

- You need high flexibility

But here’s the catch:

Renting should be temporary Ownership should be the goal

₹50K Rent vs ₹50K EMI Navi Mumbai – Common Mistakes Buyers Make

₹50K Rent vs ₹50K EMI Navi Mumbai – Common Mistakes Buyers Make

Waiting.

People think:

“I’ll buy when prices drop.”

But in Navi Mumbai:

- Infrastructure is expanding

- Demand is increasing

- Supply is getting absorbed

Prices are not dropping significantly

So every year you delay:

- Property price increases

- Your EMI potential increases

- Your affordability decreases

Smart Strategy (What You Should Actually Do)

Smart Strategy (What You Should Actually Do)

Instead of overthinking, follow this:

Step 1: Check Your Budget

If you’re already paying ₹50K rent, You can likely handle ₹50K EMI

Step 2: Choose Growth Location

Focus on areas near:

- Metro lines

- Airport influence zones

- Business hubs

Step 3: Start Small if Needed

Even a 1BHK today can become:

Your stepping stone to bigger investments

Step 4: Work with a Genuine Agent

A real expert:

- Saves you from bad deals

- Finds undervalued properties

- Negotiates better pricing

Final Truth: It’s Not About Rent vs EMI – It’s About Mindset

People who stay renters:

Think short-term comfort

People who buy:

Think long-term wealth

And that’s the real difference.

Understanding ₹50K rent vs ₹50K EMI Navi Mumbai can completely change how you build wealth over time.

Rent vs EMI Navi Mumbai – What Should You Choose in 2026?

Rent vs EMI Navi Mumbai – What Should You Choose in 2026?

Also read our guide on hidden charges while buying a flat in Navi Mumbai to avoid unexpected costs.

In the end, the

rent vs EMI Navi Mumbai decision is not about affordability – it’s about financial awareness.

If you’re paying ₹50K rent in Navi Mumbai in 2026,

you’re already financially capable of building an asset.

The question is not affordability.

The question is awareness.

Because:

- Rent disappears

- EMI builds ownership

- Property builds wealth

And in a city like Navi Mumbai,

this might be your once-in-a-decade window before prices climb even higher.

If you’re still stuck between ₹50K rent vs ₹50K EMI Navi Mumbai, now is the time to make a smarter move.

The post ₹50K Rent vs ₹50K EMI – One Builds Landlord’s Wealth, The Other Builds Yours appeared first on .